Looking Ahead

It may well be that America may have reached its zenith a decade ago. We are now clearly on the downslope as we face the confluence of several apparently unstoppable economic forces. These include the growth of government spending beyond its means, the need to be able to support the interest on our debts, the aging of our population, and the cumulative effects of previous over-consumption. Any one of these things would be disabling by itself, but now we have multiple and simultaneous driving forces that could well bring economic results approaching those of the Great Depression and the inflation of the Carter years--combined.

I ask you to consider the factors below. Some of the effects can be reduced, but not eliminated. Others are almost as certain as the sun will rise in the morning and set in the evening.

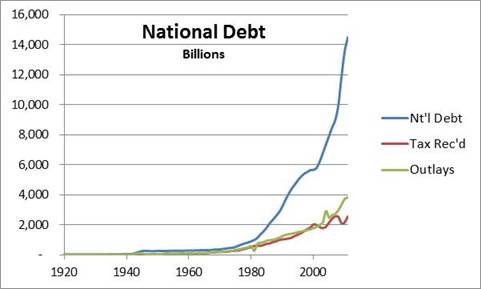

Government spending beyond its means is self-evident. Every federal budget dollar now requires borrowing 40% to make the cash payments. Unlike the high debt from World War II, much of that debt is held by foreigners, China in particular. This debt must be rolled over as the government bonds mature. That means that the interest rate must be competitive with that of comparable securities. In the past, we have enjoyed the enviable position of having the most secure bonds in the world so there was little need to worry about competition. The downgrading of our debt may be controversial since we are still the world’s currency as a practical matter. Still, it is a statement of fact that we have gone so far, and have done so little to stop the debt growth, that our ability to both attract more lenders as well as to pay the interest are more than “concerns” and a “threat.” They are real and here now.

The need to support the interest on our debts is so important that a debt payment failure is equivalent to unthinkable bankruptcy. We need to borrow more money in order to sustain defense, discretionary spending, entitlements, and the cost of government itself. The federal debt of more than $14 trillion now exceeds $100,000 dollars per household. That debt is far understated because of the way the Congress keeps books. Unlike private businesses which are required to hold trusts for pensions and account for future payments in their books, the government does not include the future obligations for entitlements such as Social Security, Medicare, Medicaid, unemployment compensation and government pensions. Federal debt and unaccounted obligations exceed $600,000 per household.

But our individual debt problems don’t end there. Personal debt now is well over $100,000 per household. Few people facing retirement have the $300,000 for the medial costs per household during retirement. All told, the average household in the U.S. has more than $700,000 of debt while most of those around retirement are not prepared for another $300,000 burden.

The current approach in Congress does little to stop the plunge! The administration, like administrations before it, created commissions to recommend corrective actions, and, like previous administrations, has refused to accept the commissions’ plans that would do much to abate our future problems. We are now on a course of miniscule reductions in the rate of debt growth, not the debt itself. The administration alone is not to blame. The Congress does not have the political strength and will to risk reelection by taking the necessary action—which is equivalent to the kind of things private businesses do to survive. That is, cut spending on everything by large percentages. Further, the leadership must set the example by cutting their own compensation, perks, staff, travel, office space, and so forth.

As examples, Boeing had to make a 60% labor reduction that ended in 1971 when a large billboard in Seattle read, “Will the last person leaving Seattle—turn out the lights.” I headed the Boeing Aerospace Company in the early ‘80s when we had to cut our labor force by 40% to survive. Those are kind of actions that must be made just to stop increasing the federal debt, not reductions of a couple of percent

The aging of our population means more support for the elderly and fewer workers to provide the income to support this. Aging has been well underway for more than a generation as birth rates have declined and life expectancies have increased. After the soldiers came back from World War II, 77 million baby boomers were born and are now starting to reach retirement age. Demographers tell us that the number of children required to sustain population is about 2.13 children per woman. We are well on our way to go below that as people marry later (if at all) and decide to have no or just two children. Many women prefer to stay in the workforce or bear children much later in life meaning many others would have to have more than 2.13 children on average. The birthrate in Europe is 1.38. Japan’s is 1.2. Russia is 1.17.

Then there is the increase in life-expectancy. Life-expectancy is the average death age in the population, that is, 50% will live longer and 50% will die sooner. When Social Security was started, few people were expected to reach the age of 65 because life-expectancy was so low. Now, large numbers of people reach 65. Once at 65, the male life-expectancy is 86 and female life-expectancy is 88. More important, 25% of 65 year old males will live to 91 and females to 93. Joint life now is more than 91 for the surviving spouse and 25% of spouses will live to be more than 95.

Improved medical services, drugs and technology have been major contributors to longer lives. They also have increased the cost of medical care and associated entitlements. Medicare and Medicaid reimbursements to doctors and hospitals often cover only a fraction of the actual costs. The number of doctors who will not accept Medicare patients continues to grow. Medical school graduates often have loans that exceed their home mortgages. This drives medical students to seek the higher paying specialties and away from general practice where the shortages are acute. De facto rationing already exists and will have to increase as more people are brought into entitlement programs. The theory is that more people with Medicare and Medicaid will therefore have longer lives.

The combination of a lower birth rate and extended lives means fewer people to support the entitlements of the aged. According to Third Way, in 1990 there were 3.9 taxpayers for every retiree. In the following ten years, that dropped to 3.6. Third Way estimates that in the next 20 years, there will be only 2.6 workers for every retiree. Said another way, in 2010, the number of those more than 65 was 24.6% of the population between ages 25 and 65. The Bureau of Economics estimates that will increase to 36.3% by 2025. Per these estimates, the elderly will be more of a problem to support by 1.48 times (36.3%/24.6%) in just 15 years! That means that the burden of paying for entitlements will increase by almost 40% using Third Way numbers and 48% using government age projections--and that assumes that the entitlements per retiree do not increase per current legislation! Nor is there any allowance for the fact that almost 50% of wage earners pay no income tax.

Finally, there is the burden of previous over-consumption. Consumption is the opposite of saving. You either spend or you save. You don’t do both with the same dollar of income. People started living beyond their incomes. They bought houses they could not afford; they added ever-more desirable entertainment purchases; utility bills sky rocketed with the advent of cable; education bills soared, and so on.

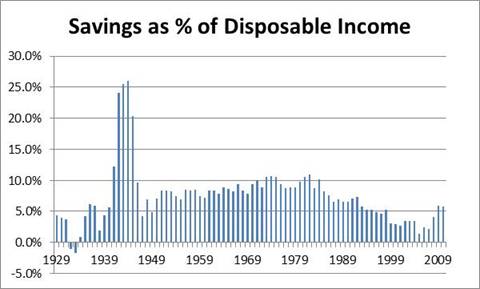

After World War II and until 1985, people, on average, saved about 9% of their disposable income. Disposable income is gross income less income taxes. Starting in 1985, the national savings rate started its steady decline. In 2005, it reached a negative 0.5%. Political redefinitions to “chained” values in later years revised the 2005 value upwards to a plus 1.4%. Chained values are based on things such as substituting hamburger for steak, but that is not a measure of constant life style. Now the chained savings rate has increased for recent years to a little over 5% now--far from that required to sustain retirement.

Employers, government excepted, stopped pension plans and put the burden on the employees to save for their own retirement with 401(k) plans or equivalents. The national savings rate should have gone up, not down during those decades by what could have been another 5%.

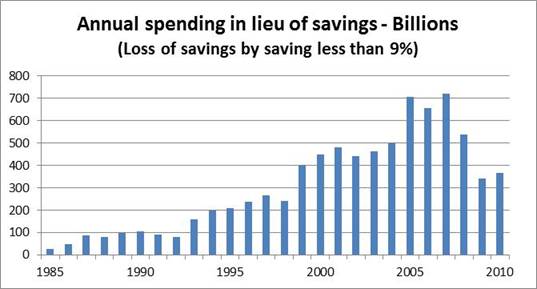

Ignoring the pension shortage, the difference between what people actually saved and a steady 9% savings exceeds $8 trillion in lost personal savings. (See the figure below.) If invested in 50% bonds and 50% stocks in each of those years, the equivalent savings loss would exceed $15 trillion. That is an amount bigger than the reported national debt. It’s also at least as deadly as the national debt because it means that workers who are saving too little will have to save more, and those who are retired will have less to spend. This is contrary to what the government, industry and financial firms want us to do.

Then there are people who find saving anything very difficult. Paul Farrell’s article, Tax the super-rich, 8/15/11 on MarketWatch.com, lists the following statistics: “one in five Americans [are]unemployed or underemployed. One in nine families [are]unable to make the minimum payment on their credit cards. One in eight mortgages [are] in default or foreclosure. One in eight Americans [are] on food stamps.”

The Employee’s Benefit Institute Research’s 2011 report found that less than 56% of workers and 54% of retirees have saved less than $25,000 not including home equity. Worse, 29% of workers and 28% of retirees have saved less than $1,000 not including home equity. Home equity, once used to justify low savings, now should be left out of retirement plan entirely per many financial planners.

More than half of families don’t have enough savings to buy a new car, pay for major dental work or a roof replacement and a burial site—nor can they offer financial help to their elderly parents who have run out of money or temporarily support their divorced daughter with young children, much less normal living expenses, or worse, long-term-care. These are destined to be poverty stricken in old age.

So we are facing a population that is aging and therefore requires longer lifetime support as well as increased medical costs--without adequate savings for retirement! The government, industry and the financial firms want people to spend more, not save more. Though more spending will make the national economy look temporarily better as measured by Gross Domestic Product (GDP), it will really be getting sicker and sicker. The number of unemployed combined with the increased number of elderly forms a formidable voting block that clamors for more entitlements, not the necessary entitlement reductions needed to keep the government solvent. Almost 50% of wage earners pay no income tax and will continue to support welfare and generous entitlement programs. Government is growing faster than industry. Government unions provide major support to politicians who then become beholden to the unions. Politicians are reluctant to reduce labor costs and retirement obligations.

Looking ahead, what will happen? Of course none of us can predict the future. Hopefully we will not see rioting or worse. But one thing is for sure. Our children and their children will pay heavily for our over-consumption, excess government spending, and the support of an aging population. They will do this with some combination of high taxes and inflation. Inflation is the traditional way that the government has paid its past debts with cheaper dollars, and that debt looks smaller when measured in less valuable future dollars. What’s very different than tradition is the extent of entitlements—all of which increase with inflation so that inflation does nothing to make those obligations smaller.

Inflation means that lenders will demand higher interest rates. Interest rates now are far below historical averages. As they rise, interest payments on the national debt can easily exceed what we spend for national defense. The government makes economic forecasts and scores congressional measures using low future interest rates and a generous and continued expansion of GDP. The real costs of government programs will grow appreciably because we will have neither low interest rates nor low inflation.

Tax rates will have to increase, especially considering the reduced number of tax-paying people relative to those receiving entitlements. The number of things to be taxed and the methods of taxation will grow at both federal and state levels. An addition of a value-added- tax and/or a much simplified tax return, perhaps without deductions and credits, might help somewhat, as would higher tax rates for the superrich—paradoxically who actually now pay most of the taxes but often at lower effective rates than middle income Americans. And a simplified tax structure would help the rest of us who have to spend hours, if not days, gathering tax information.

Increases in inflation and taxes mean that personal and commercial interest rates will have to increase as well. Rate increases mean that bond fund principal will go down. People with adjustable rate mortgages (ARMs) will pay heavily, many losing their homes, thereby adding more to the welfare roles. Industry will have to increase prices because of higher taxes, higher labor costs, higher benefit costs, and higher financing costs. None of these things bode well for the economy.

Only a few will escape this dismal fate. They are those who have saved and invested with an eye on the future. They are those who will not panic during abrupt downturns. They are those who have maintained good health practices. They are those who have a good support network both for work and for retirement. They are those that pay attention to the economy and government actions. They are the workers who want to learn new things and have multiple job skills. They are the elderly who spend below their income and have reserves for emergencies. They are those that know how to live on very little income as did many of our ancestors during difficult times.

I urge you to consider the things above and plan for contingencies. Take appropriate actions both financially and health wise. Importantly, prepare your children and help them to learn about financial matters, skills needed for employment in turbulent times, the things that drive politicians, and, particularly, that consumption is the opposite of saving. Benjamin Franklin got it right: “A penny saved is a penny earned.”

Henry K. (Bud) Hebeler

8-18-11